Hello,

Long time no see. In the last few weeks there have been more and more articles about the AI bubble being inflated. And while that is true, it seems to completely ignore that nearly everything else in the US market is absurdly valued as well. Liquidity is extremely high, with Bitcoin being where it is and bubble stocks being inflated - even outside AI.

In the meantime, for many companies fundamentals have stalled or worsened and the US is reigned by a guy who changes his mind on tariffs faster than a squirrel trying to hide its winter supply. Germany, Austria, Denmark, Italy, France and Sweden and the Japan Post won’t deliver mail to the United States due to the tariffs.

And yet the US market has bubbled higher. So today, I am going to write about exactly that - and that the market has completely removed any notion of disbelief - being now the biggest stock market bubble in history. In the past the stock market used to be a leading indicator for the economy. However, due to passive index investing and that it is in the government’s best interest to keep it up, it has become a lagging one.

On Friday Trump changed his mind yet again, so many bubble stocks cratered - as well as Bitcoin, but they are still at extraordinarily expensive levels.

The AI Bubble

That AI is in a bubble is nearly impossible to disprove now. It’s multiple times the size of even the subprime mortgage bubble before the Great Recession.

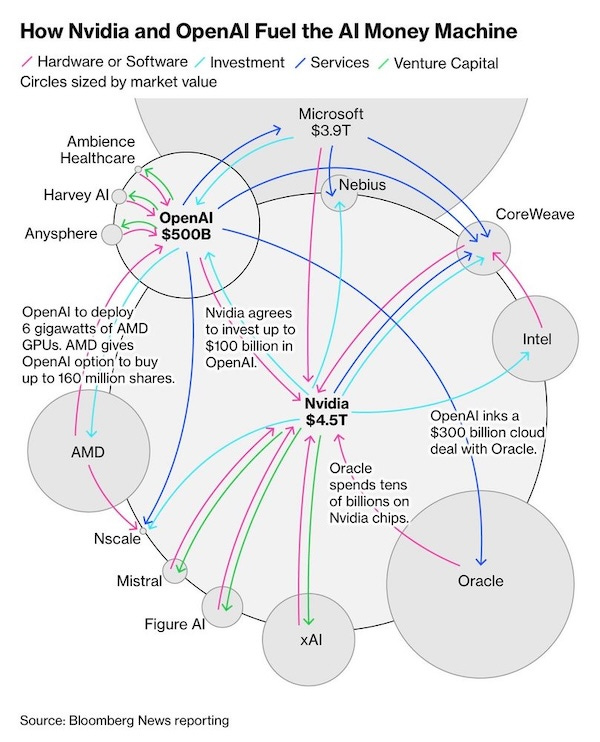

What is more is that it is extremely circular. Everyone is investing in everyone - boosting their own demand.

OpenAI with 4.3b revenues in the first half of 2025 announces an investment/partnership with AMD and the stock went up 101b at one point on that news. Nvidia is now at 4.5 Trillion in market cap. OpenAI spent more on marketing and equity options than it made revenue in the first half of 2025.

Oracle’s projected backlog shot the stock up to over 1 Trillion in market cap. There is no consideration for the amount of hundreds of billions of dollars that are required for those data centers especially as the company has now negative Free Cash Flow and a Total Debt / EBITDA ratio of over 4. The stock jumped over $400b being promised $60 billion a year from OpenAI, an amount that OpenAI doesn’t earn yet, to provide data enter facilities that Oracle haven’t built yet. At the same time they had a double miss in earnings and revenue estimations.

The thing is that the more I actually use AI, the more skeptical I am of its real life usage. It has a big problem with consistent data, often making stuff up - and even when linking it correct resources or documentation it often ignores it. While I am sure that AI will be used a lot in the future, I don’t think it will be as much as the current projections indicate. If you look at the cover of this post it should become clear - it can’t even properly generate text.

Coreweave (who rents out Nvidia graphics cards) still with loses of 290m due to interest expenses and is of course valued at over 70b. If they can’t make money now, when will they be able to?

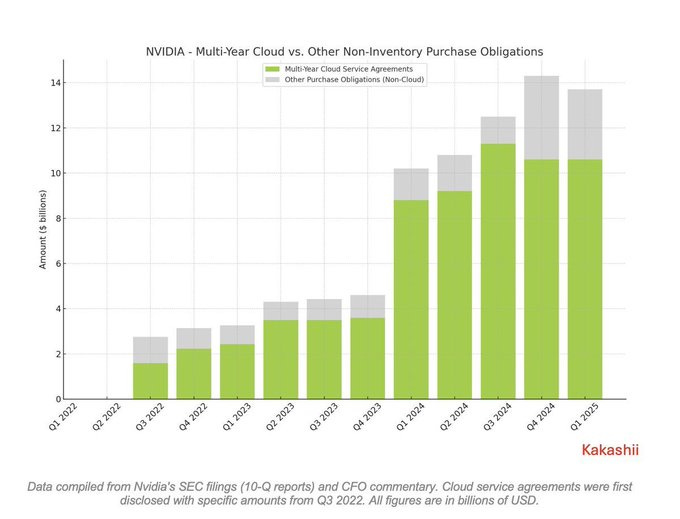

Given the insane sums that range into the trillion, there isn’t enough capital to do all that is promised - yet stocks act like there is. Commits to purchase is now treated as “has already purchased”. Enron used to call that mark to market accounting.

The ARKK / pipe-dream bubble

After years of outflows, Cathie Wood seems to be back. Having had their biggest single-day inflows since 2021 in the last few weeks. Palantir has overtaken Johnson & Johnson in market cap at one time and is now at around 420b in market cap. 140x P/S and yet hardly anyone can answer what they do - a throwback to Mark Minervini being asked about Upstart in 2021.

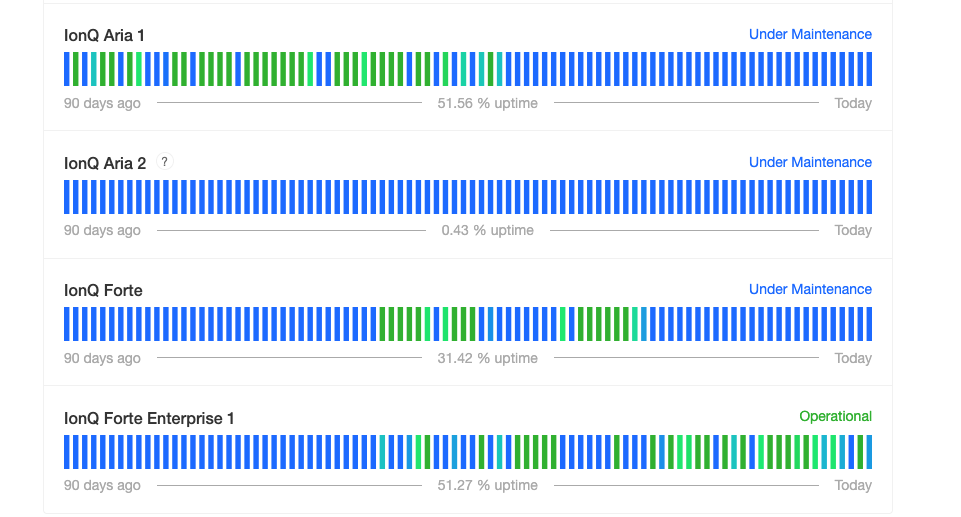

Quantum stock companies have surged to seemingly no end. Rigetti, IonQ etc have risen to 15b and 23b. With press releases like: “we expect Oracle Cloud Infrastructure revenue to grow 77% to $18 billion in 2025 and then increase to $32BN, $73BN, $114BN, and $144BN over the subsequent four years”. At the same time the tech doesn’t work. The downtime of IonQ quantum computers have been excessive - with one having 0.43% uptime the last 90 days.

Joby - a flying car company has overtaken Subaru, Renault and Xpeng in market cap and is now valued at 10x their projected 2030 earnings. There are so many of those companies out there, its nearly impossible to count them all. Many with a fervent retail following that could be nearly considered a cult.

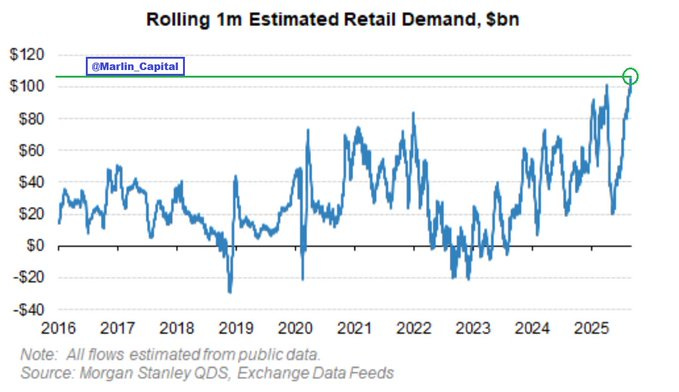

Retails is also just buying. Call option volumes is at new highs, retail call demand is surging. There is no end.

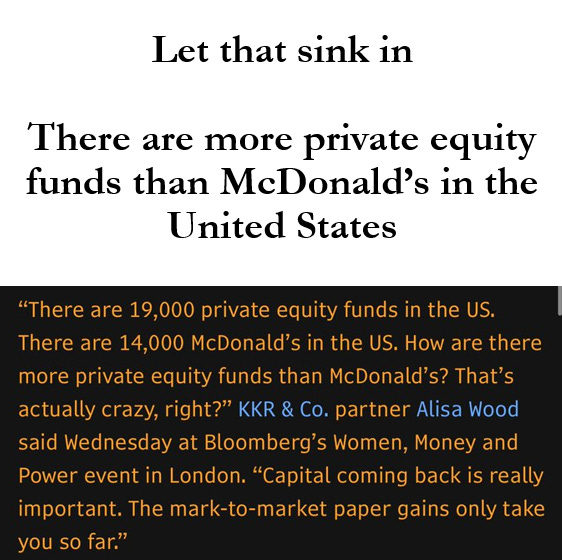

Private Equity

Not having daily prices seems to be a new trend.

Tesla

There is probably more to write about Tesla than a reasonable book could fill. From the insane proposed 33b salary for Musk in the next years (that he will get without hitting any targets, which is 80% of the cumulative net income from Tesla), to the deteriorating fundamentals, slowing sales, damaged brand reputation and finally competition - it doesn’t look good. Fundamentally that is. The stock is doing fine being at 17x P/S and 1.4T in market cap for a car company, that if it weren’t for carbon credits would have posted an operating loss in Q2.

The new “affordable” model costs 3000$ more than the old costed last week with tax credits. On that the stock gained 75b in market cap. More than Mercedes, BMW and VW. Given that the tax credits were 7500$ that means that Tesla is having its profitability by car cut down by 4500$ each. Pipe dream isn’t a strong enough for the delusion that is Tesla stock.

Everything else

The thing is that nearly all companies trade at exceptionally high valuation. Apple is close to its highest valuation in history, with barely any growth. Costco, Walmart etc as well. Microsoft has questionable accounting with their AI investments.

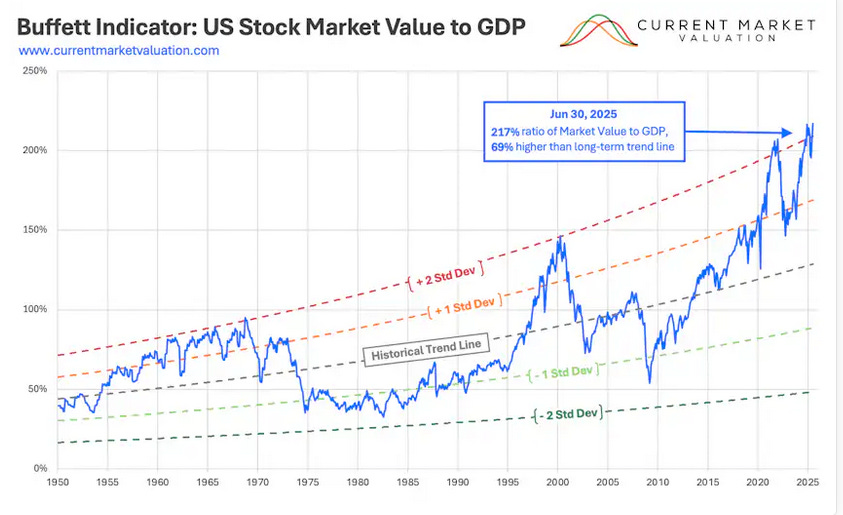

The Cap to M2 is its highest since the Dot-com era and the Buffett indicator is well above the historical trend line.

There also is now an insane concentration risk. Nvidia now represents over 5% of the MSCI All Country World INdex. That is higher than Japan’s 4.78%, while China, the UK and Canada account for 3.33%, 3.23% and 2.92% respectively. It ‘s contribution to the index is now larger than France and Germany combined. I would not call that an All Country index.

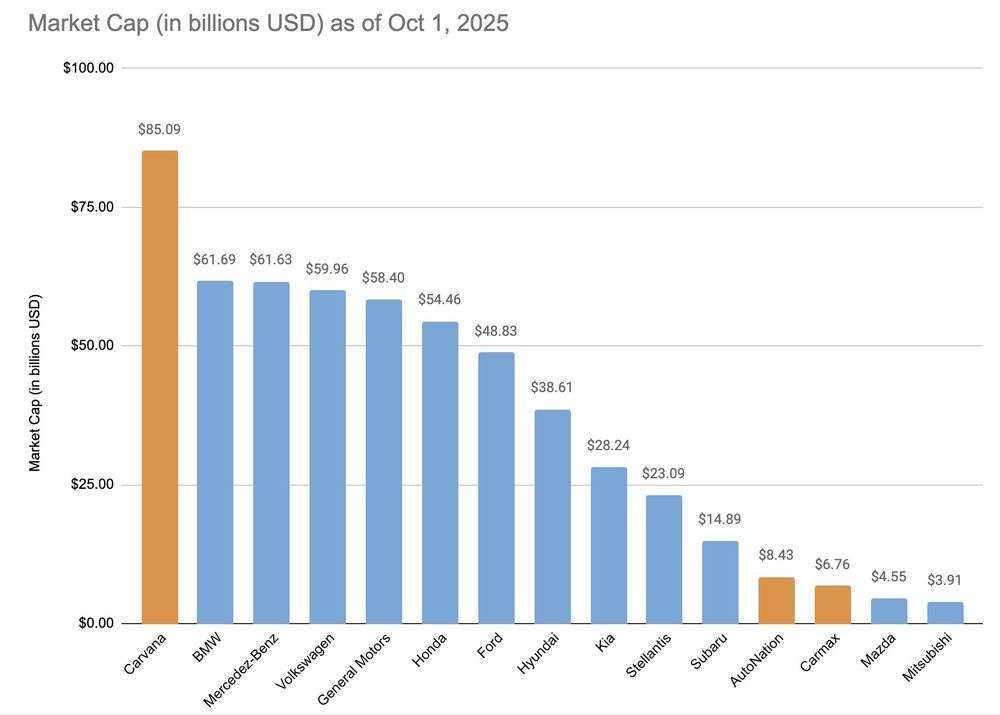

Then there are dozens of companies like Doordash or Carvana that seem to ignore every reasonable valuation metric to their business model and are around 50-150b in market cap. (Given that the total used car market profits are 9b - including small dealers).

What baffles me as well is that numbers that companies put out are taken at face value. For example Meta puts out a number that estimates how many users it has in total (DAP = daily active people). That number is not the total number of user accounts, but their estimate of unique people using at least one of their products - and they state that their margin will be 3% of their worldwide DAP. Meta is putting that number at 3.48b. So if we take the Chinese population and people without internet, we only have 4.1b left. That means that they 84% of the total remaining worldwide population use meta daily? And that is without taking into account children or elderly - that is a very optimistic number. But I haven’t found a single analyst or public person question this number.

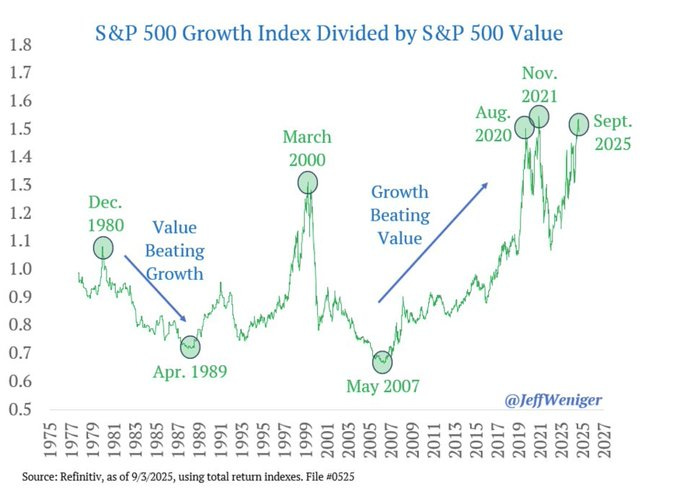

The ratio of S&P 500 Growth to Value in the US has hit a new record high, surpassing the peak of the meme stock bubble in 2021.

If we go with P/S, P/EBIT, P/FCF and ROCE. These are all more expensive now than they were during the dotcom bubble.

The tariffs are already putting a strain on farmers. Last year China bought 47% of the US produced soy beans, this year it is zero. The US administration did spent 20b on Argentinian debt tho, who is the biggest exporter of soy to China after they stopped buying from the US. One doesn’t need to have a history degree to forecast what happens when farmers struggle.

Furthermore so far in 2025 companies have announced nearly 1 Million job cuts, the highest since the pandemic year of 2020.

How long will the bubble last - nobody know. I have bought a few 2027 puts.

There are so many companies that are extraordinarily cheap in the rest of the world. Why bother with a market where the fundamentals as much as the truth does with the current US administration?